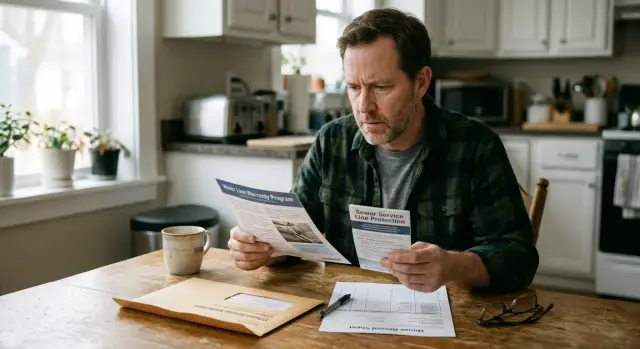

Water line warranty scam signs in property-based mailers

Learn why a water line warranty scam can look routine when mailers use ownership records, home age, and line details to sound official.

Why these notices seem ordinary

Most of these letters do not look suspicious at first. They look familiar, and that is the whole idea.

They often use your real name, street address, and details tied to the property. When a letter mentions a real water line, sewer line, or exterior service line, it feels less like junk mail and more like something you were supposed to get.

Timing does a lot of the work. Many people start seeing these notices soon after buying a home. That makes them easy to believe. New owners expect a flood of paperwork, warranty offers, utility updates, tax notices, and maintenance reminders. One more envelope about buried pipes does not seem unusual.

The design helps too. These mailers often feel official without clearly being official. They may use blocky layouts, muted colors, account-style numbers, reply slips, or phrases like "final notice" and "service interruption." None of that proves the sender is your utility. It just borrows the look of a bill closely enough to lower your guard.

Another trick is sounding specific while staying vague where it counts. A letter may say homeowners are often responsible for the line running from the house to the street. In many places, that is broadly true. Because one part of the message is true, the whole pitch can feel routine even when the company behind it is unknown.

That is why these offers fool careful people too. The sender does not need a wild story. It only needs a few real facts and a familiar format.

What scammers learn from property records

A lot of scam mail does not start with a hack. It starts with public records.

County and city records often show enough detail to make a sales pitch feel ordinary. That is why a water line warranty scam can sound oddly specific on first contact. The sender may know your name, your address, and a few facts about the house.

The details are usually simple: owner names from deed or tax records, the year the home was built, the sale date, and parcel facts like lot size or home type. None of that proves the sender knows anything about your actual water or sewer line. It only means they found data that is public, cheap to collect, and easy to sort.

A recent sale date is especially useful to bad actors. New buyers are still learning what the city covers, what the homeowner covers, and which notices are real. A letter that arrives a month after closing can feel like one more dull piece of home paperwork. That is exactly the effect the sender wants.

Year built matters too. If a home was built in 1958, 1974, or 1991, that date helps the sender sort you into a list and guess which worries might work. They do not need to inspect anything. They just need enough detail to sound believable.

Parcel records add another layer. A detached single-family home on its own lot is a better target for certain mailers than a condo, since the owner is more likely to think about private exterior lines. Even lot size can shape the message. A longer run from house to street sounds more expensive, so the warning feels more personal.

The part many people miss is scale. These lists are often pulled in bulk, cleaned up, and reused. One company, lead seller, or scammer can sort thousands of homes by age, owner, and purchase date, then send nearly identical letters with tiny edits. That is why the mail feels personal when it is really mass-produced.

If a notice seems to know a lot about your home, take that as a reason to slow down, not a reason to trust it.

How home age turns into a pitch

A house built in 1968 sounds different from "an older home." One detail makes a mailer feel less random. It sounds like the sender knows your property, and that alone can make people read it like routine paperwork.

Home age is easy to turn into a worry. Pipes, shutoff valves, and sewer lines do wear down over time. The problem is that low-trust sellers take that ordinary fact and stretch it into a near-term threat, even though they have not seen your plumbing.

An exact build year makes the pitch feel informed. A letter that says your home was built in 1974 can seem almost official, especially when the envelope looks like utility mail. In most cases, that year came from public property records, not from an inspection, a repair history, or access to your utility account.

The logic is simple. Your home is older, so failure must be more likely. Repairs can cost thousands, so a small monthly fee feels safe. The offer sounds time-sensitive, so you feel pushed to act fast. And because the build year matches your house, the warning feels personal instead of mass-produced.

That leaves out a lot. Age alone does not tell you the pipe material, past repairs, soil movement, tree-root pressure, or how well the line was maintained. A well-kept house from 1955 can have fewer line problems than a poorly maintained house from 2005.

That is why this pitch works so well. A homeowner gets a letter with the exact build year, a scary repair estimate, and a low monthly price. The price feels easy to accept, and the matching year makes the sender seem informed. Sometimes that is enough to pull someone into a water line warranty scam.

Age is a clue, not proof. When a pitch treats home age as a direct path to failure, it is trying to turn a normal fact into pressure.

How mailers and calls borrow the look of a utility

A lot of these pitches work because they do not look like ads at first. They look boring and routine, which is exactly why people open them.

The envelope may say "urgent" or "final notice" in large type. That creates the feeling that you missed a payment or ignored a utility issue. For an older homeowner, or anyone juggling bills, that small jolt of stress can be enough to lower their guard.

Inside, the letter often copies the layout of a bill. It may show an account-style number, a service address, a response deadline, and a payment box. None of that proves it came from your water company. It only makes the offer feel familiar.

That is a common move in a water line warranty scam. The seller wants you to think this is part of normal homeownership, like electric service or trash pickup, not a separate product you should stop and question.

Calls use the same trick. The caller may already know your name, address, and sometimes the age of the home. Then they ask you to "confirm" those details, which makes the conversation sound official. In reality, they may just be reading from property data and trying to pull you along.

The pattern is usually the same. The message sounds urgent. The design looks like a bill. The caller already knows a few facts. And the real nature of the offer is buried in tiny print.

That last part matters. If you slow down and read the fine print, you may find wording like "this is a solicitation" or a statement that the company is not your utility provider. That line is often there because it has to be. It is just placed where many people will miss it.

The safest rule is simple: if it looks like a utility notice, prove that first. A real provider does not need vague branding, bill-style design, or pressure language to explain what it is.

What these offers are actually selling

Most of these mailers are selling a service contract, not water or sewer service from your utility. That difference matters. The company is usually offering to pay for certain repairs if a private line fails, under rules it wrote.

That can sound close to a normal utility bill or city program, which is why the pitch works. The envelope, logo style, and urgent wording can make a private contract look official.

The fine print is where the real product shows up. Many plans have a payment cap, waiting period, deductible, or narrow repair rules. Some exclude pre-existing damage. Some will not cover a full replacement if the pipe is old, crushed, or blocked by roots. Others pay for the pipe repair but not the cost of digging up a driveway, sidewalk, or landscaping.

Before you buy, check how much the plan will actually pay, what damage is excluded, whether there is a waiting period, whether excavation and surface repair are included, and who chooses the contractor. Those details decide whether the plan helps at all.

Another point gets buried on purpose: your city or utility usually is not requiring you to buy this. A public utility may send general notices about homeowner responsibility, but that is different from telling you to purchase a private plan from one company. If the mailer sounds mandatory, be skeptical.

Responsibility for a line also depends on where you live. In one town, the owner may be responsible for the line from the house to the street connection. In another, the split may happen at the meter, curb stop, or another point. That is why a generic letter that says every homeowner needs this protection should raise questions.

Some of these plans are real contracts. But real does not mean required, and it does not mean useful for your home. Read it like a product offer, not like a city notice.

A simple example of how someone gets pulled in

Three weeks after closing on her first house, Nina gets a letter that looks routine. Her name is correct, the address matches the deed, and the mailer notes that the home was built in 1974. Those details often come from public ownership records, but to a new buyer they can feel personal and official.

That is what lowers her guard. The envelope says "Final notice," and the letter warns that buried water and sewer line repairs can cost thousands. The monthly price looks small, so the risk seems bigger than the bill. It never clearly says it is from the local utility, but the design and wording get close enough that she keeps reading.

She calls on a lunch break. The person on the phone sounds practiced, not pushy at first. They mention older homes, aging underground lines, and surprise repair bills. None of that sounds made up. A 1974 home really might have older pipes, and underground work really can get expensive.

Then the pressure starts. The caller says it is smart to enroll now because waiting could leave her exposed if a problem shows up later. They ask for payment details before she checks her closing papers, reads her homeowners policy, or calls the utility herself.

This is how a weak sewer service pitch pulls people in. It uses true-looking facts, familiar paperwork, and just enough fear to make a rushed decision feel reasonable.

New owners are easy targets because everything is new at once. Mail is arriving every day. Bills are changing. Accounts are being set up. When a letter sounds like one more normal house task, many people pay first and verify later.

That is the trap. The details make the offer sound routine. The rush keeps the person from checking whether it is routine at all.

How to check a mailer or call step by step

The safest move is simple: slow down. These offers often work because the mailer looks routine and sounds urgent, so people respond before they verify anything.

Start with the document you already trust, not the mailer in your hand. Your real water or sewer bill usually shows the correct customer service number, your account details, and the name of the actual utility.

- Do not call the number printed on the mailer or given by the caller. Put the notice aside and pull up your latest water or sewer bill instead.

- Call the utility number from that bill and ask one direct question: "Am I responsible for the line they mention, or is the utility?" Responsibility changes by city, and scammers count on people not knowing.

- Check your homeowners insurance before you buy anything. Some policies already cover certain service line problems, or offer a rider for less than a pushy mailer suggests.

- Search the company name on its own, then with words like "complaint," "refund," "claim denied," or "misleading mailer." One bad review means little. A repeated pattern means much more.

- If the offer came by phone, ask them to mail the full terms and stop there. A real business can wait.

One more check matters: ask what is actually being sold. Some offers are not repair service. They are service contracts with exclusions, waiting periods, or claim limits that people only notice after a problem starts.

If the answers stay fuzzy, walk away. A real utility problem can be checked through your bill, your insurer, or your local office without trusting a stranger's number.

Mistakes that make people trust the offer

A common mistake is treating public facts like proof. A mailer may show your name, street address, year built, or a note that you own the home. That can feel official. It is not. Those details are often easy to pull from property records or data broker files, so a water line warranty scam can sound routine even when it is just a sales pitch.

People also trust the format too quickly. The envelope may use dull colors, blocky text, and phrases that sound close to a city utility or county office. Some calls do the same thing with scripts like "this is about coverage on your service line." If you do not stop and ask who is selling what, a paid offer can blur into what sounds like a required notice.

Another mistake is paying during the first call. Pressure works because the amount often looks small enough to feel harmless. Someone thinks, "It is only a few dollars a month," and gives a card number before checking whether the company is tied to the local utility at all. That first payment is often the whole goal.

People also give away more information than they need to. Once a caller confirms your full name, phone number, email, and details about the house, they can make the next pitch sound even more convincing. For sewer service scams, that extra information can turn a vague script into one that feels oddly personal.

Short deadlines are another trap. "Reply by Friday" or "final notice" creates enough stress to shut down basic checking. Real utility issues usually give you a clear way to verify the notice through your normal bill or service account, not by rushing you into a phone payment.

A quick checklist before you respond

A lot of these letters work because they look boring, not dramatic. They arrive with your name, your address, and just enough home details to sound normal. That is why a water line warranty scam can pass as routine mail if you read it too fast.

Before you call, pay, or scan anything, stop for two minutes and check the basics:

- Look at the envelope first. If the sender name is vague, hidden in tiny print, or different from the name used inside the letter, treat it with caution.

- Do not use the phone number printed on the mailer until you verify it another way.

- Search the fine print for words like "solicitation" or "offer." Many mailers count on people missing that one line.

- Check whether the price, coverage limits, exclusions, and waiting period are easy to spot.

- Confirm whether you already have coverage through homeowners insurance, a home warranty, a service line rider, or a local utility program.

One small detail matters more than people think: how hard the offer makes you work. A real provider should make the terms easy to read. If you have to hunt for the cancellation policy, the repair cap, or when coverage starts, the letter is telling you something.

Calls follow the same pattern. If the person pushes urgency, mentions your property age, or says a problem is "common in homes like yours," slow down. Ask for the full business name, callback number, and written terms.

If they resist any of that, put it aside. A decent offer can wait until you verify it.

What to do next if your data keeps feeding the pitch

If the same kind of mailer keeps finding you, do not treat each letter or call as a separate annoyance. Treat it as a data trail. Someone keeps pulling your name, address, and home details from places that are easy to search, copy, and resell.

Start by keeping a small record. Save the mailer, take a photo of the envelope, and write down the date, phone number, company name, and anything specific they mention about your home. Patterns matter. If the same details show up across different offers, that tells you your information is circulating widely.

A few simple moves help. Ask the sender where they got your property details. Ask whether they bought your data from a broker or marketing list. Ask them to stop contacting you and note the reply. Keep records of repeat calls, especially from new numbers.

Most people stop at blocking a number. That helps for a day, not for long. The bigger fix is reducing how much personal data is exposed on broker sites. Those sites often combine public ownership records with extra details like past addresses, relatives, phone numbers, and estimated home age. That is what makes these pitches sound believable.

Pay extra attention after a home sale or a move. Contact usually spikes then. Fresh ownership updates, forwarding data, and listing history can make you look like an easy target, especially if a caller assumes you are still sorting out utilities and home maintenance.

If you want less manual work, Remove.dev helps remove personal data from over 500 data brokers and keeps monitoring for re-listings. That will not erase public property records, but it can cut down the extra profile data that makes these mailers and calls feel personal.

If a notice knows too much about your house, the next step is not to argue with the offer. It is to shrink the data trail that keeps feeding it.

FAQ

How can I tell if a water line notice is real?

Start by checking your real water or sewer bill, not the number on the mailer. If the letter looks like a bill, uses words like "final notice," or hides "solicitation" in small print, treat it as a sales offer until your utility says otherwise.

Why does the letter know my home's build year?

That detail often comes from public property records, not from an inspection or your utility account. A correct build year can make the letter feel personal, but it does not prove the sender knows anything about your actual pipes.

Am I always responsible for the line from my house to the street?

No. Responsibility changes by city and sometimes by the exact point where the line connects. The safest move is to call the number on your normal utility bill and ask where your responsibility starts and ends.

Are these mailers always scams?

Not always. Some are real service contracts, but they are still private products, not required utility service. Even when the company is real, the plan may have waiting periods, exclusions, or low payout caps that make it a poor fit.

What should I check before I buy one of these plans?

Read the full terms before you pay. Check the repair cap, waiting period, exclusions, whether digging and surface repair are covered, and who picks the contractor. Then compare that with your homeowners policy or any service line rider you already have.

What should I do if a caller asks me to confirm my address and property details?

Stop the call and do not confirm more details than they already have. Ask for the full business name and written terms, then end the conversation and verify the company on your own.

Why do new homeowners get these offers so often?

A recent home purchase makes you easier to target because you expect a lot of paperwork and do not yet know which notices are routine. A letter that arrives soon after closing can blend in with real bills, tax mail, and setup notices.

Can my homeowners insurance already cover service line problems?

Sometimes, yes. Some homeowners policies include service line coverage or let you add it for less than a pushy mailer suggests. Check your policy first so you do not pay twice for similar protection.

What if I keep getting these letters and calls?

Save the mailers, note the dates and phone numbers, and ask senders where they got your information. Blocking one number may help for a day, but reducing how much personal data is exposed through data brokers usually does more over time.

How can Remove.dev help with property-based scam mail?

Remove.dev helps remove personal data from over 500 data brokers and keeps watching for re-listings. It will not erase public property records, but it can reduce the extra profile data that makes these offers feel unusually personal.